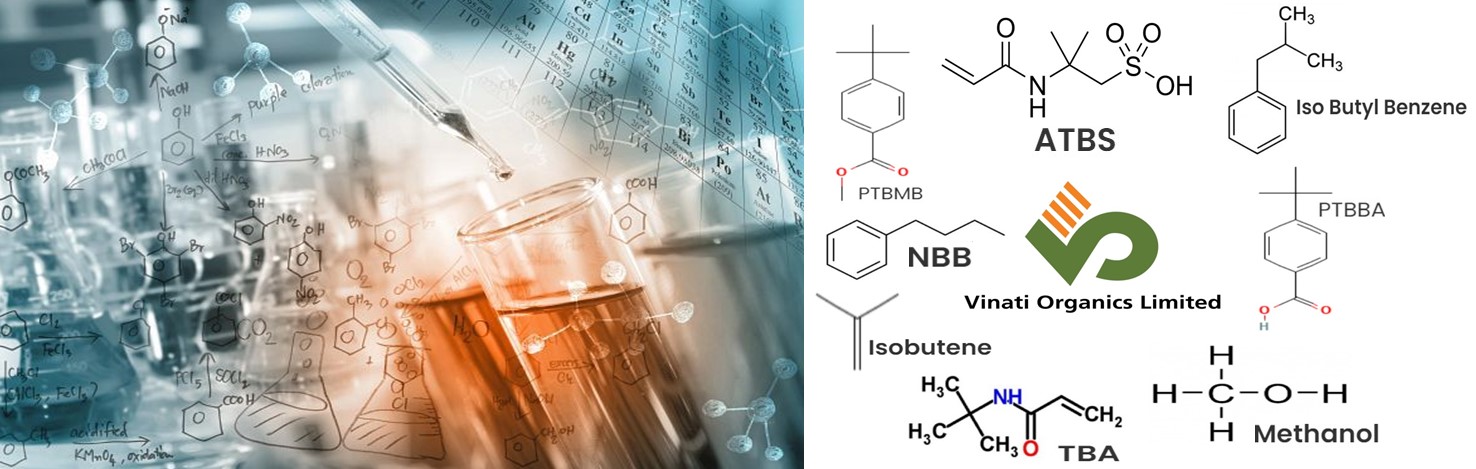

Vinati Organics Ltd – Amplifying Value through Undiluted Market Leadership in Niche Integrated Business in FY23 & Beyond.

Founded in 1989, Vinati Organics Ltd. (VOL) Integrated Business Model has helped it to transform from a single product company to one of the world’s largest manufacturers of key specialty chemical products, while serving the customers across the globe.

As a market leader for key specialty chemicals (especially for ATBS & IBB where it commands more than 65% of global market share), VOL products play a very important role for several downstream industries. As such company is on the track to further expand its Niche Portfolio of products, which will enable Import Substitution and Create Superior Value for all the Stakeholders.

Vinati Organics is among the few companies in the sector with Sustained capacity expansion with Low-Gearing. This is a result of Prudent capital allocation and Disciplined cost management, resulting in high cash generation.

Hence company’s market capitalisation has grown by 49x between March 2012 to March 2022, while it was expanding its product portfolio through strategic CapEx all funded by the internal accruals.

It has become a consistently Free Cash Flow (FCF) generating Growth Engine which may last forever, given the multiple industries which VOL’s products caters to and the Structural Tailwinds to the Specialty Chemicals sector which Vinati Organics operates in.